A Tale of Two Shores – a 2012 Retrospective

There was so much noise coming out of Washington in 2012 about the fiscal cliff, budget deficits, taxes and especially jobs that these topics became the primary conversation at many a holiday cocktail party. Over the past few weeks I’ve been asked about the current state of offshoring vs. onshoring at least a half a dozen times. Some of the inquisitors have come from a reasonably informed perspective, while others have attempted to cloak the issue of onshoring in some form of sociological or moral high ground related to the U.S. workers’ entitlement to jobs. While pondering the complex issues around outsourcing/offshoring this holiday season, I could not help but think of a few apropos, although completely unrelated, words from Charles Dickens.

It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity......

Despite the occasional high profile example, or smoke and mirrors-laced press releases in 2012 from the likes of Dell and others, the general state of, and trajectory for, manufacturing in the U.S. today is not appreciably different than it was a year ago. Major shifts in industrial production patterns tend to follow long-term, secular economic trends, and are only influenced marginally around the edges by short-term changes and political issues. Yes, there is a bit more talk of late in the U.S. about nearshoring and onshoring of manufacturing; but the outlook for a dramatic resurgence of domestic production in 2013 driven by a massive repatriation of offshored manufacturing is something Dickens also addressed quite eloquently.

…. it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before U.S., we had nothing before U.S., we were all going direct to Heaven, we were all going direct the other way…….

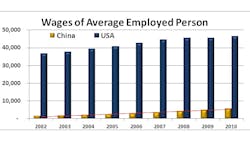

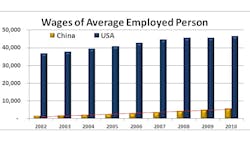

Many of the people I talk to about reshoring production are quick to point out the dramatic rise in labor costs and other factor input costs in China as a giant catalyst for manufacturing repatriation. The rise in costs in China over the past decade have been considerable – especially in U.S. dollar terms as the yuan has appreciated considerably against the dollar since the summer of 2005. At a gross country level, the average wage of all employed persons in China has risen by about 260% over the past decade, while the equivalent macro number for the U.S. is about 26%. All of this talk among manufacturers about rising costs in China needs to be taken in context. The average employed person in the U.S. still makes more than eight times what the average employed person in China makes. When viewed relative to U.S. wages and the rate of change of U.S. productivity, Chinese manufacturing is still extremely attractive for many products despite the headline wage inflation.

China, like most geographically large countries, exhibits a pretty broad range of wages across regions and provinces. This pattern is not entirely dissimilar from the pattern that we see in the U.S. where wages tend to be higher on the coasts. Arguably the geographic variation in wages is significantly broader in China than the U.S., but this gap will likely close dramatically over the next decade or so. Many OEM’s and manufacturing services firms that are heavily invested in offshore manufacturing are starting to look for alternatives to the more developed and more expensive areas of China. But most of these firms are looking to either Western/Central China, or lower cost locations in Southeast Asia and not the U.S. 2012 was a year where some production returned to U.S. shores from China, but this represents jut a very tiny fraction of total offshore production. There is no massive rush to repatriate manufacturing jobs back to the U.S. and 2013 – 2015 will not look appreciably different in this respect.

China Offers More Than Cheap Labor

But wages are just one part of the manufacturing equation and in more and more cases, wage differentials and labor arbitrage is no longer an import factor. China has emerged as the world’s electronics factory over the past 15 to 20 years, and has positioned itself well to defend its dominance with far more than just cheap labor. Those of you that follow me on Twitter (thanks mom) will know that next year China will become the world’s largest user of industrial robots. The country has also developed an incredibly diverse and robust supply base for virtually all of the components and raw materials that go into today’s modern electronic products and an increasingly skilled and experienced technical workforce to support these activities. Today an individual company’s consideration of possibly re-shoring widget production back to the U.S. is complicated by the fact that most of the components for their widget are built in China.

I asked Mark Mondello, Jabil's long tenured COO, and recently appointed CEO, for his thoughts on rising costs in China and how they are influencing manufacturing strategy for his company and its clients. Mondello said “Clearly costs in China have risen over the last five years and we see that trend continuing, but for each and every product, each and every customer, and each and every end market served, there are a multitude of variables that need to be considered when deciding on global supply chain solutions. These are complex issues that we model every day and that impact customers very differently.” The number of interrelated variables impacting manufacturing location decisions does indeed make this a complex issue and one that is influenced by a number of different macro trends.

Perhaps the most influential counter-trend to a dramatic reshoring of production to the U.S. is the emergence of increasingly attractive consumer markets in Asia. It is very true that the size of the cost reductions to be realized by outsourcing production to China has slowly and steadily contracted over the past seven years; but during that same period the attractiveness of Chinese production to satisfy Chinese consumption has steadily and dramatically increased. Over the past five years or so, the U.S. consumer has become somewhat tapped out while the consumer in China has been doing some serious consuming. From 2007 to 2010, total U.S. household spending rose less than the rate of inflation (it contracted in real dollar terms), while household spending in Vietnam, Indonesia, and Malaysia all grew in the double-digits. During that same period, the world’s largest consumer base in China grew household spending by more than 25% (see bubble sizes in figure 2). To put this into a geo-economic perspective, in three years’ time, both Malaysia and China each expanded household consumption by an amount roughly equivalent to the entire household consumption of Austria.

U.S. Remains Attractive Market

The explosive growth of the emerging market consumer in Asia has more than made up for the slightly diminished attractiveness of China as a new or incremental outsourced manufacturing destination for western OEMs. Hungry for both top line growth and gross margin expansion, more OEMs are starting to look at the opportunity to service highly attractive emerging markets as part of their calculus around where they will place their outsourced manufacturing. This is not to say that U.S. manufacturing is finished, or even that the exodus of manufacturing jobs from the U.S. will continue unabated – this is just not the case.

I asked Mondello for his observation on U.S. manufacturing jobs and reshoring, figuring a guy with 140,000 manufacturing employees in 20 countries probably has some pretty good insights here. On the topic of reshoring Mondello said “…some manufacturing jobs are coming back to the U.S. ever so slowly. This will continue for the coming years and may possibly accelerate depending on cost curves, politics, and trade relations. Today we see the United States as a primary player for innovation, engineering creativity, logistics solutions, and leadership - we see China as the primary player for manufacturing. China still has the most efficient indigenous supply chain, especially when considering electronic hardware.” The innovation engine that is the U.S., the sheer size of our not quite flat world, and our 308 million consumers insure that there will always be a meaningful manufacturing base in the U.S.

Despite anemic growth of late, the U.S. is still a pretty darn attractive market. The tapped out consumer households in the U.S. still consume four times more dollar value of goods than the households of China, despite that country having a population well over four times that of the U.S. And despite the prevalence, and in some sectors the outright dominance, of outsourcing as a model for production, much of the manufacturing being outsourced to China today is clearly done so without a comprehensive analysis of the total costs of so doing. Every day my firm sees OEMs that have outsourced production offshore only to perpetually struggle with managing their outsourced supplier. In many cases companies realize a six to 10 point reduction in Cost of Goods Sold (COGS) on paper, which very quickly gets offset by a two to three point increase in Other Cost of Goods Sold (OCOGS) and the “peanut butter” spreading of another couple of points in ever expanding Opex. Despite all the advances in tools and systems for communication and collaboration, managing production half a world away from sales, product development and product line management functions can still present significant challenges – none of which are without cost.

2012 was clearly a year where the offshore/onshore debate was a tale of two shores. But much like the tale of those two cities chronicled by Dickens more than 150 years ago, the contrast between the two is very much in the eye of the beholder. So what did I say over a few cocktails to those holiday party goers looking for my seemingly informed opinion on the “shoring” and manufacturing jobs debate?.Hey, how about those 49er’s!!

Contributing Editor Ron Keith is chief executive officer for Riverwood Solutions, a supply chain consulting and managed services firm.

About the Author

Ron Keith

Chief Executive Officer

Ron Keith brings more than 24 years of operations experience to Riverwood Solutions including engineering, manufacturing and executive management positions at Westinghouse, Wavetek, Rockwell, Alcatel and Flextronics International. Ron has a reputation as an innovator, team builder, creative problem solver and strategic thinker who delivers straight talk and strong results to Riverwood's clients. He has run international EMS operations with annual sales in excess of $1.4B and has managed manufacturing, product development, and program management personnel in numerous countries.

Ron has advised more than four dozen companies on their manufacturing operations, supply chain, and outsourcing strategy including more than a dozen Global Fortune 500 companies. He has previously consulted for four of the top 10 EMS (Electronic Manufacturing Services) companies and has advised hedge funds, private equity funds and strategic investors on a number manufacturing services related investments. Ron has published more than 30 articles on various manufacturing, technology and business related topics including strategy, operations, quality management, technology trends, and supply chain management.

Prior to founding Oreamnos Partners and Riverwood Solutions, Ron served as Vice President and General Manager at Flextronics International, where he started and ran several divisions in both the EMS and ODM (Original Design Manufacturer) spaces during his more than eight year tenure. He worked with, and ran manufacturing operations for, a number of leading OEMs at Flextronics including Cisco, Motorola, JDS Uniphase, Nortel. W.L. Gore, Kyocera and others.

Ron has undergraduate degrees in both Electronic Engineering and Manufacturing. He received an MA in International Management and an MBA in Operations Research from the University of Texas at Dallas, where he also completed the majority of coursework towards a Ph.D. in Organization, Strategy & International Management (OSIM).