Economists Present Predictions for 2017 San Diego Economy

At the 33rd Annual San Diego County Economic Roundtable, a panel of experts discussed the future of the national and local economy, workforce development, the housing crisis, and innovation in education. I have been attending these roundtables since the early 1990s and was a panelist myself three years ago, so I always enjoy catching up with people I know. This annual event was held at the Joan B. Kroc Institute for Peace & Justice at the University of San Diego.

The roundtable was sponsored by the County of San Diego, the San Diego Workforce Partnership, The San Diego Union-Tribune, and the University of San Diego School of Business. The moderators were Roger Showley and Phillip Molnar of The San Diego Union-Tribune. This year’s panelists were:

- Gina Champion-Cain, chief executive officer, American National Investments

- Matt Doyle, assistant superintendent, Innovation, Vista Unified School District

- Alan Gin, associate professor of Economics, USD School of Business Administration

- Tina Ngo Bartel, director of Business Programs and Research, San Diego Workforce Partnership

- Ray Major, chief economist, SANDAG

- Deborah Ruane, executive vice president, chief strategy officer, San Diego Housing Commission

Introductory remarks were made by Jaime Alonso Gómez, the new dean of the USD School of Business, Jeff Light, editor-in-chief of the Union Tribune, and Andy Hall, vice president and chief program officer of the San Diego Workforce Partnership (SDWP). The SDWP is the local non-profit Workforce Development Board, designated by the city and county of San Diego to fund job-training programs that empower job seekers to meet the current and future workforce needs of employers in San Diego County.

Dean Gomez commented that the USD School of Business "is working to create the future, to change and be the architects of the future. We have a goal to become a $250 billion economy. We are creating bridges from the present to the future. We are educating for the present and the future. The future is here."

Jeff Light said that he had a great respect for economists, but he kept running into more and more CEOs who didn't have the same high regard for economists. So, a few years ago, they added CEOs to their local opinions on the San Diego economy [U-T Econometer]. He said, "I went back and looked at how we did last year, and both groups were very, very impressive. Last year's predictions were pretty good by both groups, but surprisingly, the CEO's did a little bit better than the economists."

Andy Hall said, "It is not cheap to do business in San Diego. It's not cheap to do business in California. We exist to close the skills gap and create career opportunities for all San Diegans, but particularly for underserved communities." He said that it is not just the training they provide, but also the conversations they initiate and connections they make that are important.

We are younger, richer, and better educated than the rest of the nation. Our $220 billion GDP would rank 26th if we were a state.

—Ray Major

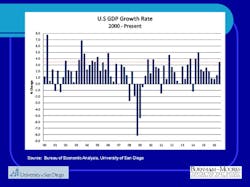

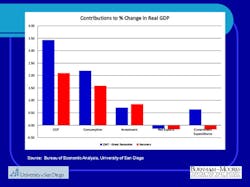

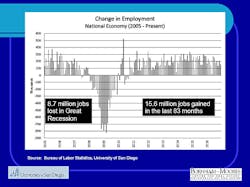

The first presenter was Ray Major, chief economist of the San Diego Association of Governments (SANDAG). He said, in part, "San Diego region is very well positioned for continued prosperity. San Diego County is the fifth largest county in the country. We are younger, richer, and better educated than the rest of the nation. Our $220 billion GDP would rank 26th if we were a state. We have a very forward-looking economy. It took 78 months for San Diego to recover from the recession from the trough in January 2010 to June 2014. The driving sectors in San Diego are innovation (10%), tourism (12%) and military (8%). Construction was the hardest hit during the recession. Construction and manufacturing are still well below what they were in 2007." He noted that construction is still down by 20% and manufacturing is down by 16%. He said that the supporting sectors of health and law, education, and government seemed to be immune to the recession and continued to grow substantially from 2009 to the present. He added, "The innovation sector continues to thrive. Military is expected to expand its presence, and manufacturing will continue its steady recovery." For 2017, he forecasts a 2.7% GDP growth, 2% inflation, higher interest rates, and 40,000 new jobs.

He touched on the fact that it is too early to know what the effect of "Trumponomics," as he termed it, will have on the national economy. He said that Trump's proposed cuts to personal and corporate rates, infrastructure programs, increased defense spending, building up the military, repealing and replacing Obamacare, relaxing regulations, withdrawing from trade agreements, and building the wall will certainly have some effect.

Associate Professor Alan Gin focused on the national economy in his presentation and highlighted the sluggish growth rate. He said, "The big problem is that since the Great Recession, the growth rate has lagged…The average GDP growth rate from 1947 to the Great Recession was about 3.5%. While we have touched that rate for a few quarters…we have averaged a growth rate of about 2%.

During the Q&A session, I asked, "Wouldn't a balance in trade increase our GDP?" He replied that the tariffs proposed would cause a trade war with China and could hurt local companies like Qualcomm that do substantial business in China. During the break, I spoke to Gin and told him that our net trade deficits have been an average 3-4% drag on our GDP, so balanced trade would increase our GDP. I also informed him that we have already been in a trade war with China, and they have been winning.

Next, he discussed the difference between the U3 and U6 unemployment rates. He explained the low labor force participation, which in his opinion is affected by the following factors:

- Retirement of "Baby Boomers" – retiring at rate of 10,000 per day since 2011

- Less participation by students

- More people leaving the labor force because of qualifying for disability

- Ability to get medical insurance under Obamacare without working

Gin commented that there are five long-term issues we need to address with regard to the national economy:

- Reduced employment

- Globalization

- Technology - internet and automation

- "Gig" economy

- Retirement crisis

- Low level of savings

- STEM divide – education more important than ever

- Growing income inequality – significant increase since 1980s

He predicted slower growth in the national economy because of slower growth in China and turmoil in the European economy. He also predicted slower growth for the San Diego economy and was slightly more pessimistic than Major for his San Diego forecast of 2.5% GDP growth and 25,000 new jobs.

It will be interesting to see how accurate Major's and Gin's predictions will be this year. If the excitement of the business leaders with whom I am acquainted is any indication, I would say their predictions are too pessimistic, and I predict much stronger GDP growth and job creation. My next article will highlight the other presenters at the roundtable.

About the Author

Michele Nash-Hoff

President

Michele Nash-Hoff has been in and out of San Diego’s high-tech manufacturing industry since starting as an engineering secretary at age 18. Her career includes being part of the founding team of two startup companies. She took a hiatus from working full-time to attend college and graduated from San Diego State University in 1982 with a bachelor’s degree in French and Spanish.

After graduating, she became vice president of a sales agency covering 11 of the western states. In 1985, Michele left the company to form her own sales agency, ElectroFab Sales, to work with companies to help them select the right manufacturing processes for their new and existing products.

Michele is the author of four books, For Profit Business Incubators, published in 1998 by the National Business Incubation Association, two editions of Can American Manufacturing be Saved? Why we should and how we can (2009 and 2012), and Rebuild Manufacturing – the key to American Prosperity (2017).

Michele has been president of the San Diego Electronics Network, the San Diego Chapter of the Electronics Representatives Association, and The High Technology Foundation, as well as several professional and non-profit organizations. She is an active member of the Soroptimist International of San Diego club.

Michele is currently a director on the board of the San Diego Inventors Forum. She is also Chair of the California chapter of the Coalition for a Prosperous America and a mentor for CONNECT’s Springboard program for startup companies.

She has a certificate in Total Quality Management and is a 1994 graduate of San Diego’s leadership program (LEAD San Diego.) She earned a Certificate in Lean Six Sigma in 2014.

Michele is married to Michael Hoff and has raised two sons and two daughters. She enjoys spending time with her two grandsons and eight granddaughters. Her favorite leisure activities are hiking in the mountains, swimming, gardening, reading and taking tap dance lessons.