Quantifying the Financial Benefits of Quality -- the Role of Governance and Transparency

In part one of this series, we discussed the role and uses of quality and its relationship to driving financial benefits from quality. What we found was that, generally, mature organizations’ quality systems tend to focus on proactively creating value, rather than simply being relegated to compliance or improvement activities. By doing so, the quality function becomes a strategic partner and can quantify the financial value of its efforts.

APQC’s Using Enterprise Quality Measurement to Drive Business Value best-practice study indicates that holistic measurement programs that are maintained by a centralized group, report measures directly to the C-suite, and provide a high-level of organizational transparency are more likely to have higher performance. In this second article, we will discuss the relationship between governance and reporting and the financial benefits of quality.

Role of Governance

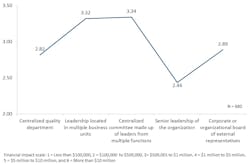

Governance determines how the organization “operationalizes” the policy established through the design, implementation, and continuous improvement of the enterprise quality system itself. Furthermore, the structure of the governing body (e.g., decentralized versus centralized) and seniority of the governing body have a direct impact of the effectiveness of the organization’s quality efforts. We wanted to take this idea of efficacy a step further and see if there was a relationship between the organization’s governance structure and the financial benefits of quality efforts (Figure 1).

Though previous research indicates that successful quality programs rely on support and guidance by senior leadership, organizations that use a centralized committee, comprised of leaders in multiple functions, see greater financial gains. This makes sense given that a cross-functional team provides a broader perspective, strengthens buy-in, and fosters adoption of quality, its benefits, and standards throughout the organization.

Reporting and Measures

Although organizations have been devising ways to measure quality for decades, many have not elevated the measurement of quality to an enterprise-wide concern. To elevate quality and its benefits, organizations need to establish enterprise-wide transparency through reporting and move to standardized measures across the business silos. Historically, most efforts focus on measuring and reporting quality within specific supply chain or product development processes, or they focus exclusively on results or finished products.

Reporting Frequency

Most of the survey respondents indicate there is standardized enterprise-wide reporting on quality measures within their organization. As reporting frequency becomes more standardized, there is an increased opportunity for real knowledge sharing across the entire organization.

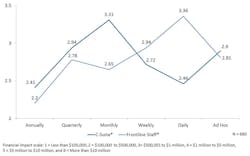

To extend this idea further and determine the “right” cadence of reporting, we tested the relationship between organizations’ reporting practices by roles and the financial benefits of their quality efforts (Figure 2).

The findings from the analysis match previous assertions that reporting measures at least quarterly to decision makers improves the efficacy of organizations’ quality programs. However, monthly reports to the C-Suite with daily reports to front-line employees tend to be associated with higher levels of financial benefits. This cadence makes sense for both roles given the nature of their involvement in decision making and their day-to-day role in meeting quality standards (respectively). However, just as important as the cadence of reporting for establishing transparency is the standardization of common quality measures in the organization.

Standardization of Common Measures

Common measures mean 1) discussions between staff (especially management) are based on a common vocabulary of performance and 2) increased sharing of practices that achieved higher performance. The majority of organizations have established enterprise-wide standards for measures of customer satisfaction, safety, on-time-delivery, and defects.

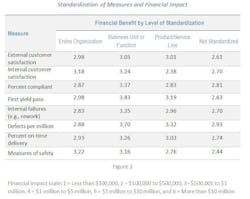

When we looked at standardization of specific measures of financial benefits, a few key factors stand out (Figure 3).

{kind=link}

Generally, standardization at some level (e.g., business unit, product line, or enterprise wide) correlates with increased financial benefits, regardless of the measure. Although it is the common thinking on the topic, the need for enterprise-wide standards is not necessarily supported by the data. The greatest impact on financial value seems to reside with standardization at the business unit or functional-level, although measures like internal customer satisfaction and measures of safety benefit from enterprise-wide standardization.

Conclusion

Similar to findings in earlier studies, quality governance models and transparency (reporting and standardized measures) do improve the efficacy of organizations’ quality efforts. Additionally, by leveraging a cross-functional governance model with reporting monthly to the C-Suite and daily to front-line workers, organizations can improve the financial benefits they garner from their quality efforts. In the next article, we will cover the relationship between quality training for suppliers and the financial benefits of quality.

Holly Lyke-Ho-Gland is process and performance principal research lead with APQC, a member-based nonprofit and one of the leading proponents of benchmarking and best practice business research.

About the Author

Holly Lyke-Ho-Gland

Holly Lyke-Ho-Gland is a principal research lead who conducts and publishes APQC research on process management and improvement, quality, project management, measurement, and benchmarking for APQC’s Process and Performance Management research team. Her research supports APQC members and clients across disciplines and centers on helping professionals and project managers solve business problems with strategy, process and measurement.