Reshoring Was at Record Levels in 2018. Is It Enough?

Part I of a three-part series.

The future of U.S. manufacturing depends substantially on our success in reducing our goods trade deficit. Eliminating the deficit will add 5 million manufacturing jobs at current U.S. productivity levels.

No other opportunities come close to offering such an impact on U.S. manufacturing and the U.S. economy. Factors such as tariffs, skilled workforce, innovation, automation and currency are all means to increase our competitiveness, thereby reducing imports and increasing exports. A lower trade deficit is the result. At a given level of demand for goods, the only way to increase manufacturing is to import less or export more. Importing less, reshoring, is far easier.

A Record 1,389 Companies Announce the Return of 145,000 Jobs

In 2018, the number of U. S. companies reporting new reshoring and foreign companies reporting FDI (foreign direct investment) was at the highest level in recorded history, up 38% year-over-year to 1,379 companies. Reshoring job announcements remained strong, at more than 145,000 jobs, reaching the second highest annual rate since we started tracking these numbers in 2007—second only to the over 170,000 jobs announced in 2017.

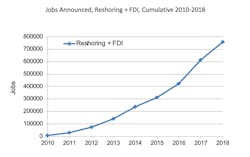

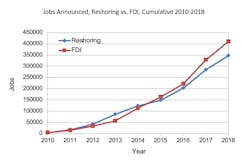

An additional 36,000 revisions to the years 2010-2017 increased the total number of manufacturing jobs brought to the U.S. from offshore to over 757,000 since the manufacturing employment low of 2010, as shown in Exhibits 1 and 2. (The revisions came from announcements that occurred in 2010-2017 but that we first discovered in 2018, as well as failed reshoring cases we learned about that we adjusted for.)

The cumulative announcements since 2010 have driven 31% of the increase in U.S. manufacturing jobs during that period and 3.3% of total December 2018 manufacturing employment of 12.8 million (conservatively allowing for a 2 year lag between announcement and hire).

The continued strength in jobs and number of companies demonstrates a tangible shift in corporate decision-making that will help drive the trends of reshoring and greater localization in the future.

The continued increases are largely based on greater U.S. competitiveness due to corporate tax and regulatory cuts, rising wages and prices in China and increased recognition of the total cost of offshoring.

Exhibit 1 | Reshoring Initiative’s 2018 Data Report

Exhibit 2 | Reshoring Initiative’s 2018 Data Report

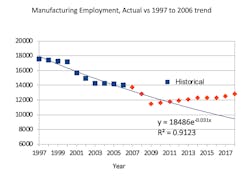

The trend in U.S. manufacturing employment, as shown in Exhibit 3, is the best evidence that a combination of less new offshoring and more reshoring and FDI is working. The chart shows a regression line based on manufacturing employment from 1997, before China joined the WTO, to 2006, before the great recession. If the trend had continued, U.S. manufacturing employment would be three million jobs lower than the actual level today. So, the trend is favorable, but so far, too slow to reduce the trade deficit.

Exhibit 3 | Reshoring Initiative’s 2018 Data Report

Trade War

Some companies in a variety of industries had been reshoring long before the current trade conflict. In many cases, it already made good economic sense. The ongoing trade dispute with China has more companies rethinking their sourcing and siting decisions. The heavy use of tariffs has caused more reshoring by companies wanting to produce or source within the U.S. tariff walls. Fifty-seven companies gave “tariffs” as a reason for reshoring. Ninety-nine percent of those were in 2016 to 2018, indicating a response to anticipated and actual Trump tariffs. “Trump” as a factor, was cited 83 times, often in association with corporate tax cuts and tariffs.

Counteracting that effect, a large number of companies cite the unpredictability of the Trump tariffs, including the steel and aluminum tariffs, as a negative: raising costs, increasing uncertainty and delaying investment. Given the size of the U.S. goods trade deficit, a uniformly higher tariff on all goods from all countries would dramatically increase U.S. manufacturing but raise prices.

Implementing a value-added tax, as used by almost all other countries, would be a better alternative. In the short-term, the spotty and unpredictable Trump tariffs are probably a net negative for reshoring and U.S. manufacturing. The results and timing of the Chinese negotiations will determine whether the effort was worthwhile.

Is Reshoring Strong Enough to Eliminate the Trade Deficit/End the Trade War?

The U.S. trade actions under Sections 301, 232 and 201 of U.S. trade law, also known as the Trump tariffs, are intended to reduce the $700 billion/year non-petroleum goods trade deficit. Can we reshore enough to dramatically reduce the trade deficit and end the trade war?

Reshoring is strong but imports and the trade deficit are still growing. Why? Partially due to the relative scale of the two trends. In 2018 cumulative reshoring grew 23% from a $110 billion 2017 base. Imports grew 6% from a $2.2 trillion base. We need to accelerate the reshoring trend enough to compensate for imports having a base that is 20 times as large.

Is the Trade Deficit Important?

Some academic economists question the emphasis on reducing or eliminating the goods trade deficit. Many believe that having a strong manufacturing sector is not important; we can all be trained to write code and provide legal services to each other. Actually, balancing the goods trade deficit would have the following essential benefits for the U.S.:

- 40% increase in U.S. manufacturing: add five million manufacturing jobs, increase capital investment by about 20% for 20 years, and dramatically increase productivity

- Significant reduction in the budget deficit

- Restoration of the middle class and SME manufacturers, resulting in reduced income inequality

- Improvement of the environment by reducing global pollution

- Strengthened defense industry base

- Reduction of the opioid epidemic (50% of those afflicted had lost manufacturing jobs, according to our sources.)

- Reduction of the industrial and financial resources that have enabled China’s rapid economic and military rise and IP theft

- Strengthened skilled workforce recruitment

- Dramatically increased domestic demand and thus GDP

- Increased R&D

Drivers of the Reshoring Trend

Reporting of factors influencing reshoring and FDI has increased every year since 2010 and indicate a heightened media interest and industry awareness of the previously “hidden” costs of offshoring, such as duty, freight, carrying cost of inventory, quality, delivery, etc.

Freight cost has always been high on the list of factors, but we expect it and green considerations to become more relevant as the new emission reduction initiative by the International Maritime Organization (IMO) is implemented in 2019/2020. This IMO effort to reduce the shipping industry’s greenhouse gas emissions by 50% from 2008 levels by 2050 will enforce a ban on ships using fuel that has a sulfur content of 0.5% or higher. This change is estimated to cost the shipping industry an additional $60 billion per year, about a 25% increase in fuel cost.

The top 10 positive domestic factors shown in Exhibit 4 highlight the strongest drivers of the trend.

Exhibit 4 | Reshoring Initiative’s 2018 Data Report

Accelerating the Reshoring Trend

The rate of reshoring plus FDI job announcements in 2018 was up about 2300% from 2010. This data should motivate companies to further reevaluate their product sourcing and plant siting, making decisions that consider all of the relevant cost, risk and strategic impacts. Policy makers can use the growth of the trend as proof that, with appropriate policies, we can bring millions of jobs back.

The Reshoring Initiative offers many tools and resources to assist companies in their reevaluation and economic developers in motivating the companies. The www.ReshoreNow.org website contains:

- Total Cost of Ownership Estimator (TCOE) for sourcing and selling

- Import Substitution Program (ISP)

- Supply Chain Gaps. Part of ISP

- Advanced Library Search to identify sales prospects that have reshored

In Part 2, we will compare and quantify the optimal government strategies and corporate behavior that can improve actual and perceived U.S. price competitiveness to accelerate the reshoring trend and reduce the trade deficit.

Harry Moser is the founder/president of the Reshoring Initiative.

About the Author

Harry Moser

Founder

Harry Moser, founder of the Reshoring Initiative, grew up experiencing the glory of U.S. manufacturing. With more than 45 years of manufacturing experience (most recently 25 years as president, chairman and then chairman emeritus of GF AgieCharmilles), Moser is a leading industry spokesman for reshoring and for developing the skilled manufacturing workforce required by reshoring.

The not-for-profit Reshoring Initiative ‘s Mission is to bring back U.S., and more generally North American, manufacturing jobs by helping companies see that, increasingly, they will be more profitable if they produce and source in or near their market.