Blockchain: The 2018 Disruptor of the Year

For bitcoin, 2017 was an extraordinary year as it documented the cryptocurrency’s stratospheric rise and unprecedented entry into mainstream dialog. Regardless of which side of the bubble debate you are on, the implications that blockchain technology may have on many industries are impossible to ignore.

In technical terms, blockchain is a decentralized database that enables trustless peer-to-peer transactions without the need for any intermediaries. In concrete terms, it means that businesses are able to pay one another and exchange assets directly without a trusted third-party. It also means that legal contracts can be established and automatically executed through what are known as “smart contracts,” which can manage agreements between two parties without the need for an outside arbitrator.

The implications of blockchain technology are far reaching, with the potential to change many aspects of business across a variety of sectors. Procurement departments are poised to benefit from many of the advantages blockchain technology brings, such as cost savings, greater data transparency and shorter lead times. What that also means, and what comes with every ground-breaking technology, is that many markets are put at risk of being displaced.

Here are a few industries we’ve identified that may have the most to worry about as blockchain start-ups begin to introduce working products to the market during 2018.

Financial Services

Several markets within the financial services sector, including commercial banks, credit card payment processors and clearinghouses, are at risk due to innovation stemming from blockchain technology. One of the most disruptive aspects of blockchain technology lies in the possibilities that arise through the use of cryptocurrencies. Cryptocurrencies, such as Bitcoin, allow businesses and procurement departments to perform several useful functions that were not possible before. For example, with cryptocurrencies, businesses can make payments to employees, customers and vendors anywhere in the world instantly without any fees. In turn, businesses can avoid the delays and added costs that occur when moving money through banks, credit card payment processors and clearinghouses. Particularly, this can save a lot of time and money for businesses operating internationally.

Currently, the number of businesses dealing in cryptocurrencies is small, but growing rapidly. This increase could start to slow the amount of money flowing through traditional banking channels over the next few years, which could in turn decrease demand and prices for those types of financial services.

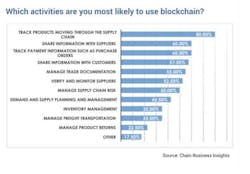

Supply Chain

Another advantage of blockchain technology is the incorruptible distributed ledger that is established with every transaction. This feature has important implications for sourcing departments and puts markets such as bookkeeping, document storage and inventory accounting services at risk. Blockchain allows businesses to track assets along the supply chain, introducing increased transparency and cost savings.

For instance, Walmart is currently piloting a blockchain program that tracks produce from farm to shelf. This tracking process not only helps keep consumers informed about where their food comes from, but can also help businesses ensure a greater level of accountability from their suppliers. Furthermore, IBM and Maersk are testing a similar program using blockchain to track and streamline shipping of a myriad of other products, which has been significantly cutting costs and eliminating delays that come with the logistics of global trade.

As blockchain technology becomes more widely implemented, we expect that several services, like the ones mentioned above, may experience decreasing demand due to the innovation in data tracking that blockchain brings. For procurement departments, it may mean cost savings, faster lead times and more transparent suppliers. Sourcing professionals should look to work with companies that are implementing blockchain into their processes.

Real Estate

Blockchain technology is poised to have a lasting effect in the real estate sector as well. We expect escrow services, notaries and title companies to feel the greatest impact. As many business owners know, real estate transactions can be incredibly lengthy and expensive. There can be brokers, escrow companies, title companies, inspectors, notaries and local government agencies involved in a single real estate deal. Blockchain technology offers a way to speed up that process and potentially eliminate the need for certain parties. For instance, by utilizing smart contracts, money can be securely held until certain conditions are met, essentially performing the same service as escrow companies for only a few cents. Furthermore, the distributed database of blockchain offers a way for information such as title history, occupancy and insurance records to be more accessible and verifiable, which will help deter fraud and theft.

Another revolutionary aspect that blockchain brings is the possibility to digitally transfer ownership of property. Securing a title now requires a piece of paper to be signed by a notary and delivered to a county database to be held. Through blockchain, property can be digitized and stored publicly, avoiding unnecessary fees and delays while also creating a more secure way to record ownership.

As such, service providers in this sector will likely also experience a drop in demand, which would translate to lower prices. Procurement departments, however, may be able to skip these services altogether as new blockchain real estate services become available, allowing buyers to stack up substantial savings in the process.

A Telling Year Ahead

Overall, blockchain technology and its effect on different sectors is still in its infancy. However, the blockchain industry is growing exponentially. While many decades-old companies race to implement the technology in their own operations, blockchain start-ups in every industry are also working to dislodge them. 2018 will be one of the first real tests to see how legacy businesses hold up against their native blockchain challengers.

Without a doubt, the landscape of many markets will change over the next few years, including healthcare, advertising and even social media. Regardless of the price of bitcoin, blockchain technology is here to stay, and which businesses are left standing will likely come down to how well companies are able to adapt. Procurement departments that are able to implement blockchain in their own processes and are actively seeking out vendors utilizing the technology will be able to reap the revolutionary benefits.

Connor DiGregorio is an analyst with IBISWorld, a provider of researched business information and market research on over 1,000 indirect procurement categories. The firm’s suite of procurement reports provide data and analysis that helps companies engage and negotiate with suppliers, better control the sourcing process, establish credibility with internal stakeholders and save money by spending smarter.

About the Author

Connor DiGregorio

procurement research analyst

Connor DiGregorio is a procurement research analyst with IBISWorld, a provider of industry and procurement research.