Lower-Tier Suppliers Must Grow To Survive

The aerospace and defense supply chain stands at another inflection point for companies, especially at lower tiers. Many face pressures to grow or get out, analysts and executives say.

With deepening demands to cut costs from end-users or aircraft and engine OEMs—as well as to fund and adopt new technologies like automation and robotics and meet commercial aircraft production rate increases and greater defense program requirements—pressures are mounting. Sub-OEM companies face a dilemma many have not encountered in recent memory, if at all.

Selling a company is one conclusive option, complicated only by finding a willing buyer and negotiating acceptable terms—assuming bankruptcy is not involved. For everyone else, there is the growing gray area of how to position a company in a rapidly evolving and intensifying marketplace.

Yet Randy Brodsky, owner and chief executive of Primus Aerospace, is more than at ease as an amorphous member of the aerospace and space (A&D) supply chain. He sees good, organic growth prospects, especially in defense, even as his Colorado manufacturing company rides the line between being a Tier 1 or 2 provider.

“I don’t ever see pressure climbing up to the Tier 1 level [permanently],” Brodsky tells Aviation Week. “It’s actually good to have a mix of both.”

Brodsky started Primus in 1989 when he bought a small metal-machining shop with about a half-dozen employees. Since then he has expanded it to a staff of 120 based at a 44,000-ft.2 Denver-area precision manufacturing and prototyping plant, with satellite offices in Arizona, Michigan and Germany. Dozens more employees are expected to be hired in coming years thanks to an exclusive contract to manufacture a new airline seat that could help cut carriers’ airport turnaround times substantially.

Among Primus’s customers are Lockheed Martin, L-3 Communications, General Dynamics, NASA, the Pentagon, United Technologies Corp. (UTC), Zodiac Aerospace, Kaman Aerospace, Textron’s Cessna and Triumph Aerospace. The company manufactures more than 500 products and assemblies each month, ranging from volumes of one unit to 50,000. Primus products are on programs such as the Boeing 787, Airbus A320, Sikorsky CH-53K, Bell-Boeing V-22, Gulfstream G series and the International Space Station.

Just a few years ago, 80% of Primus’s annual revenue was from supplying commercial aircraft and almost all of the rest from defense programs. Now, it is 70% defense and the rest commercial. “We are growing like a weed and it is almost exclusively on the defense side,” Brodsky says. But part of that growth strategy involves knowing where to fit in, not just being a certain level of provider.

“There are different ebbs and flows to the demands of the products if you’re Tier 1 or Tier 2,” Brodsky explains. For instance, a Tier 2 provider will see a downturn in a product at a different time than a Tier 1, and it faces different and usually less-direct risks related to OEMs. Also, profit margins tend to be different—and better—at the lower level.

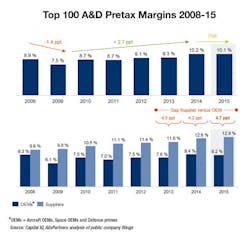

A&D advisers echo Brodsky. Boeing’s pretax margin is expected to be 8.1% this year and Airbus 7.5%. That is compared with margins ranging mostly in the 10-25% range for Tier 1 and Tier 2 suppliers, according to Fairmont Consulting Group.

This is a primary driver behind supply-chain squeezes like Boeing’s Partnership for Success and Airbus’s Single-aisle Cost Optimization Program-plus, which affect Tier 1 providers first. “The paradox of margins is driving OEMs to look toward the supply chain for cost reductions and improved productivity,” Fairmont says.

This in general follows the growth of Tier 1 providers such as Spirit AeroSystems, UTC, Honeywell and Rockwell Collins, as OEMs have turned to suppliers for about two-thirds of their sourcing. In aerostructures, OEMs also are demanding integrated suppliers and risk-sharing partners, so Tier 2 companies are consolidating to become more like Tier 1s, according to global advisory company AlixPartners.

Brodsky acknowledges that economies of scale still matter, but asserts that suppliers can generate more heft without necessarily changing tiers. “The Tier 2s have now become mammoth corporations,” he notes.

At the same time, smaller Tier 2s and Tier 3s have to adapt to market evolution and ramp-up requirements, AlixPartners says in its July global A&D outlook. Likewise, Brodsky notes that his capital investments have become “larger and larger,” especially to become automated and find enough skilled workers, but there is relatively little incentive for small businesses to do that repeatedly as tax write-offs lessen over time.

In the end, long-term visions become the deciding factor. “It depends on that company,” adds 40-something-year-old Brodsky. “If it’s a private company and you’ve got older owners, you’re going to see less investment from them. You’re going to see much more investment from younger owners like myself or private equity-backed organizations that still fall under the small-business umbrella.”

This article was originally posted on Aviation Week. Aviation Week is, like IndustryWeek, powered by Penton, an information services company.