Tales From the Transcript: Public-Company Leaders See ‘Stickier’ Inflation, Look to Offset Wage Growth

How’s this single sentence from Dover Corp. President and CEO Rich Tobin to paint a picture of where much of the U.S. economy stands in late 2023: “We’re in a little bit of a standoff in certain end markets where we would argue that inventories are down too low but we are not going to incentivize revenue into the system either through price or through terms.”

Speaking on Dover’s third-quarter earnings conference call in late October, Tobin was specifically discussing the effect of higher interest rates on distributors. But his team’s stance of holding the line on contracts illustrates a broader dynamic at work in various sectors: Consumers are looking to buy a little less than before in part because of said interest rates and because they see and hear that the economy is slowing. Meanwhile, producers’ input costs have stepped up to the point that, if they’ll do anything on price, it’s look to push through another increase.

Hence the standoff and, as we documented three months ago in our last survey of the earnings conference call transcripts of 50 members of the IndustryWeek U.S. 500 list of public companies, many executives tempering expectations about near-term growth. To that point: The Federal Reserve Bank of Atlanta’s GDPNow tool, which very early and very accurately predicted the bumper third-quarter boom of the economy, is now pointing to Q4 growth of 1.3%.

As we began doing a year ago, we scoured the transcripts of the five largest companies in 10 sectors of the IW500 to gauge leaders’ outlooks on inflation, the labor market, supply chains and demand. We rated those forward-looking comments on a five-notch spectrum from fully positive to fully negative and then calculated composite scores.

Here’s what our latest round of forward-looking data-crunching turned up, with the categories listed from most negative to most optimistic.

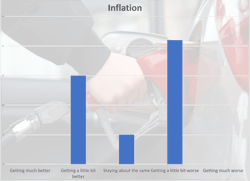

Inflation: -0.07 (-0.11 in Q2 and -0.08 in Q1)

No executive on Q3 conference calls equated inflation with the acute shocks just about everyone faced in the second half of 2022. A big factor in that is lower prices for a number of commodities, something a number of leadership teams said will really begin to benefit their bottom lines in Q1. Heading into 2024, however, the inflation pain that remains is quite chronic. Cases in point from TransDigm Group Inc. Co-COO Mike Lisman and Northrop Grumman Corp. Chairman, President and CEO Kathy Warden:

Lisman: “That dynamic doesn’t seem to have changed very much in the past few months. I know the CPI readings have come down that they publish […] We haven’t seen any kind of coming off of the prior levels really across our business.”

Warden: “We are seeing inflation be a bit stickier than we had hoped at this point in time. We are incorporating that into our forward estimates but it is impacting our ability to return to higher levels of profitability.”

Also worth noting—and there’s more on that in the very next section—is that price pressures have shifted markedly toward the labor side. That trend surfaced late this summer and grew more prevalent during Q3.

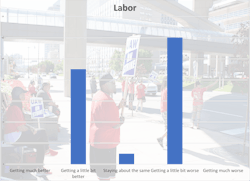

Labor: -0.07 (-0.09 in Q2 and 0.03 in Q1)

First, the good news: Most executive teams commenting on labor just from an availability perspective were upbeat. Emblematic of that common thread was American Axle & Manufacturing Holdings Inc. Chairman and CEO David Dauch: “We’ve got the bodies,” he said, even if some of those bodies are recently hired and still a drag on efficiency at times.

The less happy news: Rising wage and benefit costs—and the expectation of more increases in ’24—are weighing on margins and pushing a growing number of managers to look for offsets elsewhere in their businesses, be it via spending cuts or productivity improvements.

“The focus on reducing our direct and indirect materials, as well as our logistics cost becomes especially acute given the continued rise in labor cost across many of our markets,” Deere & Co. Director of Investor Relations Brent Norwood told analysts.

A pessimistic outlier to even that dynamic was Beacon Roofing Supply Inc. President and CEO Julien Francis: “I see the supply chain issues going away. I don't see the labor going away.”

Demand: 0.07 (0.16 in Q2 and 0.25 in Q1)

Executives’ composite view of customers’ intent to spend worsened again in the third quarter after taking a step down during the late spring. As before, our aggregate figure masks very upbeat assessments from aerospace and defense CEOs as well as (despite the United Auto Workers strike dragging into reporting season) optimism from transportation-related manufacturers with far glummer outlooks from agricultural equipment firms and chemicals and packaging execs more exposed to consumer spending.

“We know we cannot defy gravity in terms of the macro environment,” Sherwin-Williams Co. Chairman and CEO John Morikis said in late October. “What we can do is aggressively pursue new account and share of wallet opportunities to drive market share gains.”

The state of inventory destocking was a regular topic on this fall’s conference calls. The mild upbeat consensus was that many parts of the economy have stopped or are close to the end of holding back on new buys while they whittle down stock. That led to this amusing comment from AptarGroup Inc. President and CEO Stephen Tanda:

“I have several anecdotes where customers say, ‘Hey, we’re still fine, leave us alone’ and then the next week, they call out and they are, “Oh my god, we are out of stock for this item and, please, we need it tomorrow. That hasn’t happened in the past few quarters.”

A final takeaway from our demand analysis: Both our composite score and the near-equilibrium in positive and negative comments lined up very closely with what we heard early this year during the 2022 fourth-quarter earnings season. First-quarter GDP growth ended up clocking in at 2.0% after first being estimated at 1.1%—right about where GDPNow sits today.

Supply chain: 0.21 (0.20 in Q2 and 0.25 in Q1)

Three quarters of some of the highest composite scores we’ve registered across any category would suggest the supply chain snarls of the past two years have been completely untangled. Illinois Tool Works Inc. CFO Michael Larsen was emphatic in late October: “We are very much back to where we were pre-pandemic in terms of our ability to supply our customers.”

That sentiment wasn’t universal, thought: While more than two-thirds of the forward-looking sentiments we recorded were positive, we didn’t have to look far to find frustrated commentary about lead times that are still too long and parts that are still hard to secure. In the commercial HVAC division of Carrier Global Corp., Chairman and CEO David Gitlin said that’s largely a function of backlogs growing 40% over two years and said he expects those strains will soon fade.

The issues are a bit broader at Caterpillar Inc. The overall supply chain picture has brightened over the past year, Chairman and CEO Jim Umpleby said, but “some challenges and some surprises” remain. Working those—and their associated costs—out of the construction equipment giant’s system will be a high priority for 2024.

About the Author

Geert De Lombaerde

Senior Editor

A native of Belgium, Geert De Lombaerde has been in business journalism since the mid-1990s and writes about public companies, markets and economic trends for Endeavor Business Media publications, focusing on IndustryWeek, FleetOwner, Oil & Gas Journal, T&D World and Healthcare Innovation. He also curates the twice-monthly Market Moves Strategy newsletter that showcases Endeavor stories on strategy, leadership and investment and contributes to other Market Moves newsletters.

With a degree in journalism from the University of Missouri, he began his reporting career at the Business Courier in Cincinnati in 1997, initially covering retail and the courts before shifting to banking, insurance and investing. He later was managing editor and editor of the Nashville Business Journal before being named editor of the Nashville Post in early 2008. He led a team that helped grow the Post's online traffic more than fivefold before joining Endeavor in September 2021.